Often, the less time you take to pay off your mortgage, the more money you save. This isn’t an option for everyone, and lenders may not allow for shorter loan terms in all cases. But, where it’s possible, it’s a method used to pay off your loan sooner, and save on interest!

Try using the Suncorp Bank Home Loan Repayment Calculator to see how much you could be paying off your mortgage each month.

Scenario one:

Home loans are usually offered for a maximum term of 30 years. Say you buy a house worth $500,000. And say you have saved up enough for a 20% deposit of $100,000. So, you borrow $400,000. Then you chose to pay it back over 30 years with an interest rate of 4.00%p.a.

In this case, you will pay $287,478 in interest. That’s $687,478 total for the home loan and interest.

There’s nothing wrong with taking out a long-term loan. It gives you the chance to own your own home at an affordable, monthly rate. Those costs also don’t take into account the things you can save on when you own your own home. Like rent!

But, if you can afford to pay a bit more on your home loan each month, you’ll save big on interest. You’ll also get your home paid off sooner!

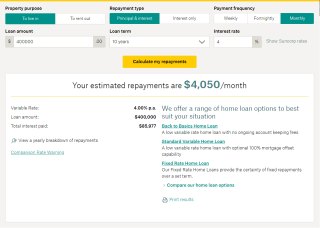

Scenario two:

If you take out the same loan as in scenario one, but pay it off in ten years, you will pay just $85,977 in interest. That’s a saving of over $200,000! The downside is you’ll have much higher monthly repayments. In this case, the monthly repayments would be $4,050 per month.

It’s something that’s not doable for everyone – and that’s fine. 25- and 30-year loans exist to help people afford their homes. But, if you can afford to rummage up the higher monthly costs – why not get your home paid off sooner, for less?

This example might not match your exact situation. Factors like if you’re buying alone or with someone, the cost of the loan, the interest rate you’re paying, and your lender’s fees and costs will all have an impact on your loan and its rates.

But what if you’re thinking of taking out a shorter home loan, or getting yours paid off quicker, but are worried about a bigger monthly fee? Then check out some ways you could be saving and paying off your mortgage faster!

- Make extra repayments

If your loan allows you to make extra repayments without incurring additional fees and charges, it could be a smart savings strategy. The more you pay off now, the less interest you’ll pay.

- Pay more regularly

If you make your repayments weekly or fortnightly instead of monthly, you’ll incidentally pay more every year. In fact, you’ll pay an extra month’s worth of repayments a year. That’ll help knock a few years off your loan!

- Don’t lower your repayment

If your minimum regular home loan repayment drops because interest rates fall, why not leave your repayments as they are, instead of lowering them?

By maintaining your current repayment, you’ll pay off your loan sooner. By doing this, you’re effectively making regular extra repayments, because you’re paying more than the minimum monthly requirements each month. You’ll be used to paying this amount already, so you won’t even notice!

- Set and forget your paymentsMany lenders, including Suncorp Bank, charge a late fee on home loans. Luckily you can also set up an automatic regular repayment from your nominated account into your home loan, so you never forgot a payment and never have to pay those pesky charges.

- Make your repayments work with your income cycleSo that you’re not scrambling for cash when your loan-repayment date is approaching, you could make it the first thing you pay after pay day. That way you’ll have a clear idea of how much spare cash you have to play with until your next pay day. That way, you won’t need to worry about making sure you have enough in the bank for your loan repayment.

- Try an offset accountOffset accounts allow you to reduce the interest you pay on your loan. Instead, you pay interest on the amount of your loan minus the balance in your linked transactions account. 100% offset accounts will have the most benefit if you go down this route. This is available on the Suncorp Bank Everyday Options accounts.

- Think carefully before choosing interest-only home loansInterest-only home loans involve only paying off the interest for a fixed period. This is instead of paying the interest and the principal. This option might give you some short-term savings, but you could end up paying more for the whole loan. This is because during the interest-only period, you’re not reducing the loan amount (principal), so you’re paying the maximum interest for that period. Interest-only home loans can be beneficial, depending on your circumstances, as they offer short-term cheaper loan repayments. Make sure to compare loan types before deciding which best suits you.

- Choose carefully between fixed and variable loansA variable rate loan could allow you to pay off your home loan sooner. Often, variable rates are lower than fixed rates. They’re also usually more flexible and can allow for additional repayments at no cost. But fixed-rate loans can offer a feeling of comfort and help with budgeting. By knowing you have a rate locked in for a certain amount of time, there shouldn’t be any nasty surprises. By the same token, you’ll miss out on any falls in interest rates during that period. Make sure to study up and choose a loan that suits you.

Find the right home loan option for you

Suncorp Bank has many options to help you choose your home loan confidently. Start your application online.

Published 26 March 2022

Related links and products

Handy tools

Home Loan, Personal and Business Banking products are issued by Suncorp Bank (Norfina Limited ABN 66 010 831 722 AFSL No 229882 Australian Credit Licence 229882) to approved applicants only. Eligibility criteria, conditions, fees and charges apply and are available on request. Please read the relevant Product Information Document and terms and conditions before making any decisions about whether to acquire a product.

The information is intended to be of general nature only. We do not accept any legal responsibility for any loss incurred as a result of reliance upon it – please make your own enquiries.